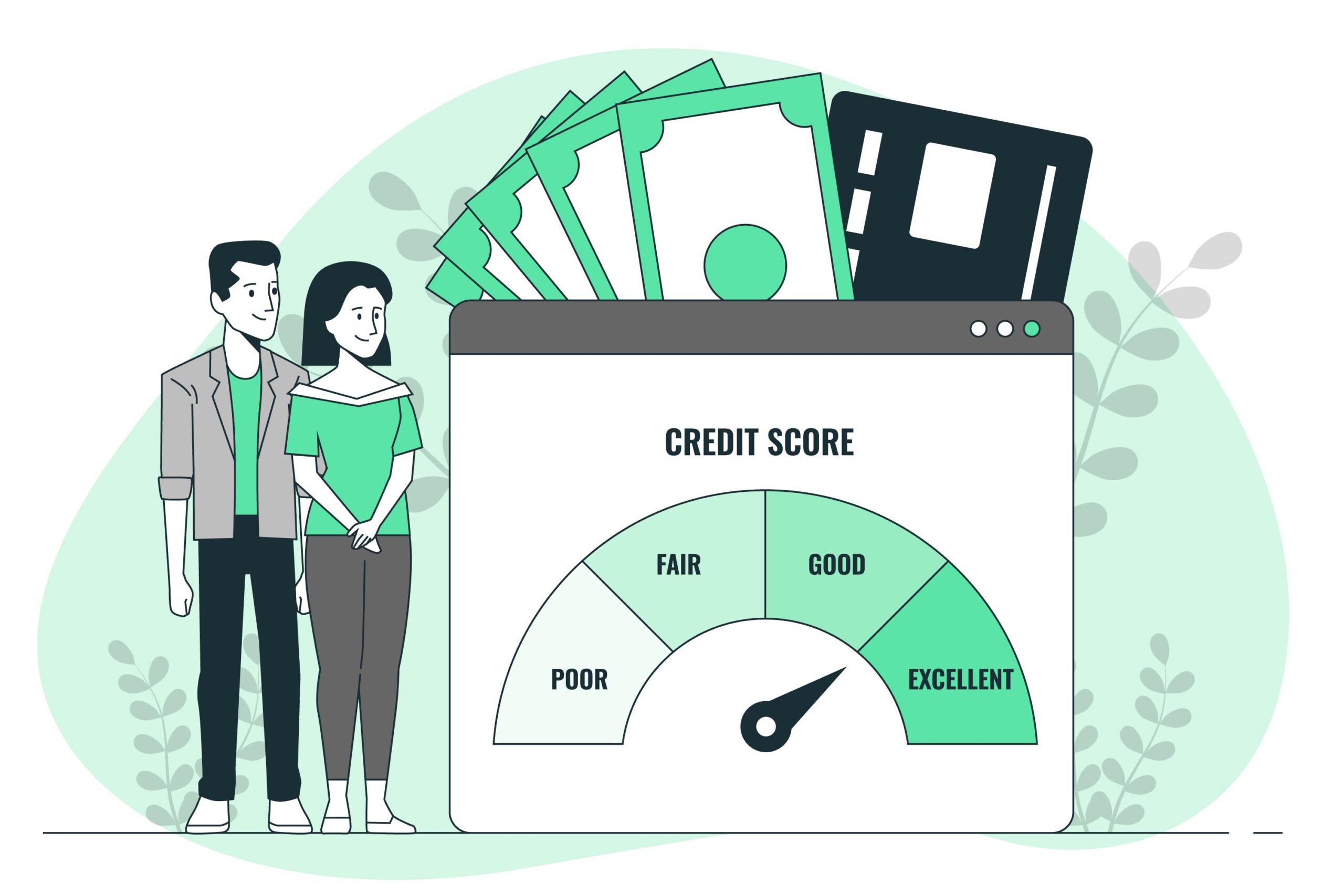

Credit Score Myths That Are Hurting Your Finance When personal finance is concerned, your credit report plays a vital part in almost every key decision—to rent an apartment, buy a house, and in many cases, land a job. Misinformation about credit scores is prevalent and dangerous, with the consequences of inaccurate assumptions quietly hurting your financial health. Here we’ll reveal credit score myths that are costing you money so that you can exchange fiction for fact and make more intelligent financial decisions.

Myth #1: Checking Your Credit Score Will Harm It

Among the most prevalent credit score myths that are costing you money is that requesting your credit report will lower your credit score. It doesn’t.

Fact: Obtaining your credit report is a soft check and will have absolutely no effect on your credit. Hard checks, on the other hand—a loan application, for instance—are likely to have a slight negative effect on your credit.

Why It Matters: Checking your credit report out of avoidance keeps you in the dark about mistakes or identity theft that will hurt your credit over time. Monitoring regularly is one of sound financial habits.

Myth #2: Paying a credit card balance increases your credit score.

One of the most prevalent myths people believe is that maintaining a balance on your credit card will help build credit. It is one of the most costly credit myths damaging your wallet.

Fact: You do not have to carry a balance to have good credit. Carrying a balance only results in interest charges. It is best to pay your credit card bill in full every month.

Why Does This Matter: Balance is bad for your utilization rate and your wallet. What builds a strong score is not debt but on-time payments made regularly.

Myth #3: Paying off old credit cards improves your credit score.

It is a common belief that canceling old credit cards will increase one’s credit score, but it usually does just the opposite.

Fact: Closing a credit card will shorten the history of your credit and raise your credit utilization rate, both of which will negatively impact your credit score.

Why It Matters: This is one of those credit myths that are quietly damaging your finances. If the card does not have annual fees, keep the account open and retain your credit history and limit usage.

Myth number 4: Your income influences your credit score

It’s simple enough to believe that higher income means a higher credit score, but that’s not the way that credit works.

Fact: Your income isn’t calculated in your credit score. Your credit behavior—the amount of debt that you have, how past payments have gone, credit inquiries, etc.—is what your credit score is based on.

Why It Matters: Mixing up income with creditworthiness may have consequences. You earn a six-figure income but a bad credit record if you handle debt badly.

How to save money 15 tips

Myth #5: Paying Off Debt Automatically Increases Your Credit Score

Another of the credit score myths that are damaging your finances is that paying debt will necessarily boost your credit score.

Fact: Paying off debt is wonderful for your financial wellness, but credit bureaus do not change overnight. Your score will not reflect these modifications for weeks, maybe a billing cycle, or two.

Why It Matters: It is disappointing to expect instant gratification. Realize that credit restoration takes time, and patience plays a crucial role.

Myth #6: All Credit Scores Are the Same

Many consumers are amazed when they discover their credit scores vary across different sources—and that isn’t surprising.

Fact: There exist a few credit scoring models (such as FICO and Vantage Score), and there are numerous versions of each. Different lenders will utilize different versions for different types of loans.

Why It Matters: Using only one credit report may be misleading before a credit application. This Credit Score Myth falls under the less obvious credit myths damaging your finances because it influences how you plan for major financial decisions.

Myth #7: Your Credit Card Alone Impacts Your Score

Most people believe that if they do not have credit cards, their credit reports will not be affected. But that is not correct.

Fact: Your credit score takes into account all forms of credit—mortgages, auto loans, personal loans, and even student loans—not credit cards alone.

Why It Matters: It’s possible that maintaining a diverse credit mix will be beneficial for your credit. Forgoing loans or other accounts deprives you of the chance to establish credit responsibly.

Additional info for credit score myths

Myth #8: It Doesn’t Matter If You Pay Late Eventually

Others think that so long as you do make a payment, your credit will not be affected. That’s not necessarily the case.

Fact: One late payment alone—30 days overdue—can lower your score considerably and remain on your credit report for up to seven years.

Why It Matters: One of the most destructive credit scoring myths plaguing your wallet right now are late payments. Many times these occur by mistake. Use alerts or automatic payments so that they do not occur.

Myth #9: You Can’t Fix Bad Credit

Most people lose hope of repairing credit because they think that credit cannot be repaired. That isn’t the case.

Fact: Credit can be repaired. Through making regular payments on time, lowering debt, and disputing errors, over time, your credit report can be rebuilt.

Why It Matters: Permanently damaging your credit score is one of the most disheartening credit myths that are negatively impacting your finances. It takes time to rebuild credit—but it’s possible.

Myth Number 10: You Don’t Require Good Credit If You Don’t Intend on Borrowing

You may think, “I don’t have a credit card or loan, so why do I care about my credit score?”—but that’s a mistake.

Fact: Your credit score influences more than lending. Landlords, insurance providers, and even employers review your credit when making decisions.

Conclusion: Credit score misconceptions have a way of harming you more than helping you if you let them. Misinformation will lead to temptation to make financial decisions that can decrease your score or keep it from increasing. By sorting through fact from fiction, you gain the ability to make wiser credit-related decisions, have a healthier financial future, and sidestep unwarranted detours. Stay knowledgeable, be skeptical of assumptions, and always use reputable sources to navigate your credit.